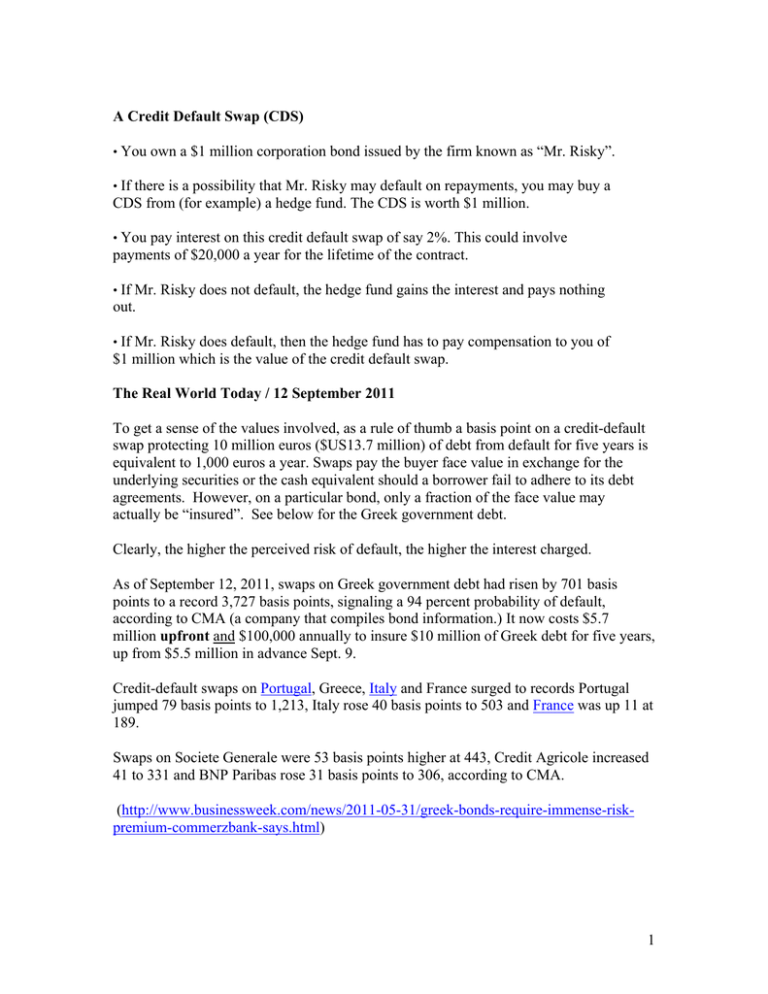

Which Best Describes a Credit Default Swap

A It is designed to reduce interest-rate risk. The ABC Bank enters into a credit default swap with XYZ Financial.

/dotdash_Final_What_Happens_When_Your_Credit_Card_Expires_May_2020-01-05392a2855bb47a6a859e3472cbe3d83.jpg)

Credit Card Definition

Which best describes a credit default swap.

/derivative.finalJPEG-5c8982d646e0fb00010f11c9.jpg)

. D It represents a way for the issuer to establish its. B The issuer receives payments from the buyer in return for agreeing to make payments to the buyer if the security goes into default. A security has no default risk exposure.

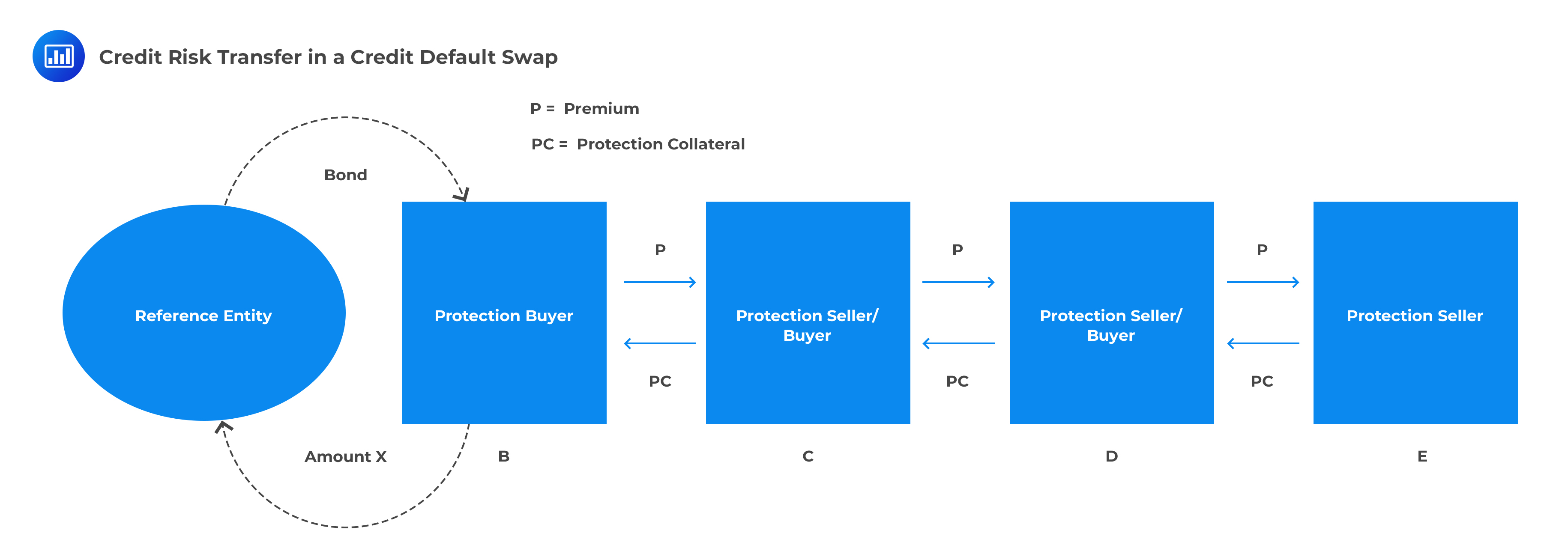

It off if another party external to the swap defaults. Credit default swap is used to transfer the credit risk exposure which arises from the fixed income securities such as bond. A credit default swap CDS is a financial derivative that guarantees against bond risk.

When credit risk increases swap premiums increaseb. It exchanges the realized return on an asset including both income and capital gainslosses for a return equal to LIBOR plus a spread on the initial value of the asset. The Correct answer is B Option ie.

They allow purchasers to buy protection against an unlikely but devastating event. Multi-credit CDS which can reference a custom portfolio of credits agreed upon by the buyer and seller CDS index. A swap designed to substitute for a basis swap.

-the principal value of the collateral underlying the contract -the market-to-market value of the contract during its lifetime -the net amount of money required to cash-settle the contract -the market price of the contract on the date it is initiated. Which statement regarding a collateralized debt obligation CDO is truea. A security represents a claim on the cash flows of a loan.

B The issuer receives payments from the buyer in return for agreeing to make payments to the buyer if the underlying security goes into default. The issuer receives payments from the buyer in return for agreeing to make payments to the buyer if the security goes into default. All of the following describe the market for credit default swaps.

Business Finance QA Library Which of the following most accurately describes the behavior of credit default swapsa. Unfortunately LMN goes bankrupt a year after this swap agreement becomes. A Credit default swap is a financial swap agreement that the seller of the Credit default swap will compensate the buyer in the event of a default.

The size of the protection payment is 5 per year. The credit default swap was created as a way for both parties to insure that neither losses an excessive amount on the investment. As of June of 2016Facebook FBhad no debtSuppose the firms managers consider issuing zero-coupon debt with a face value of 231 billion due in January of 2019 19 monthsand using the proceeds to pay a special dividendFB has 231 billion shares outstandingwith a market price June2016of 11662The risk-free rate over this horizon is 025.

When credit and interest rate risk increases swap premiums increasec. A credit default swap is an insurance policy on the default risk of federal government and corporate bonds and loans. Swaps work like insurance policies.

The CDS purchaser pay annual premium to the seller of the swap and in return collect the payment in case of default and it work as an insurance against the non-payment of the fixed liability. An insurance policy on the default risk of federal government and corporate bonds and loans. When credit risk increases swap premiums increaseb.

It carries a higher credit. The credits referenced in a CDS are known as reference entities. Which best describes a credit default swap.

C Issuers are taking out insurance in case of default. D the parties exchange principals in two currencies. Single-credit CDS referencing specific corporates bank credits and sovereigns.

It has a higher rate to compensate for the possibility of one party defaulting. It is protected against default b. A security is tax free.

Seller of the Swap. When credit risk increases swap premiums increase but when interest. B It is designed to reduce interest - rate risk.

It is protected against default. Which of the following best describes a total return swap. Which of the following most accurately describes the behavior of credit default swapsa.

A It is designed to reduce interest-rate risk. It exchanges the promised return on an asset including both income and. A swap in which the return on one bond is swapped for some other payment.

166 Credit derivatives BLM. It has a higher rate to compensate for the possibility of one party defaulting c. It allows one lender to swap its risk with another.

Which of the following best describes the national value of a credit default swap. Investments 9th Edition Edit edition Solutions for Chapter 14 Problem 27P. A credit default swap CDS is a particular type of swap designed to transfer the credit exposure of fixed income products between two or.

It carries a higher credit rating than most other swaps d. Which of the following best describes a credit default swap. The credit default swap market is generally divided into three sectors.

A security involves a credit default swapd. None of the above. It can be thought of as insurance against credit risk.

Which of the following best describes a credit default swap. 116 Which best describes a credit default swap. When credit and interest rate risk increase swap premiums increasec.

Which best describes a credit default swap. A credit default swap is an agreement between the buyer and seller to exchange the borrowers credit risk. C Issuers are taking out insurance in case of default.

That is the seller of the CDS insures the buyer against some reference asset defaulting. The swap runs for 5 years and is based upon a term loan to LMN Corp. The CDS buyer buys protection by making periodic payments to the.

A It represents a way for the issuer to establish its creditworthiness. D It represents a way for the issuer to establish its creditworthiness. When credit risk increases swap premiums increase but when interest rate risk increases swap premiums decrease.

Equity Prices Credit Default Swaps And Bond Spreads In Emerging Markets In Imf Working Papers Volume 2004 Issue 027 2004

/78293570-5bfc2b8cc9e77c0026b4f8e9.jpg)

Credit Default Swap Cds Definition

Rancilio Rocky Timer Mod Part 4 Mod2 Schneor Design And More Timer Wellness Design Diy Coffee

Pricing Of Sovereign Credit Risk In Imf Working Papers Volume 2012 Issue 024 2012

Esg And Corporate Credit Spreads Emerald Insight

Credit Default Swap Prepnuggets

Pdf What Drives The Price Convergence Between Credit Default Swap And Put Option New Evidence

Credit Default Swaps Market Gross Notional Amounts Outstanding In Download Scientific Diagram

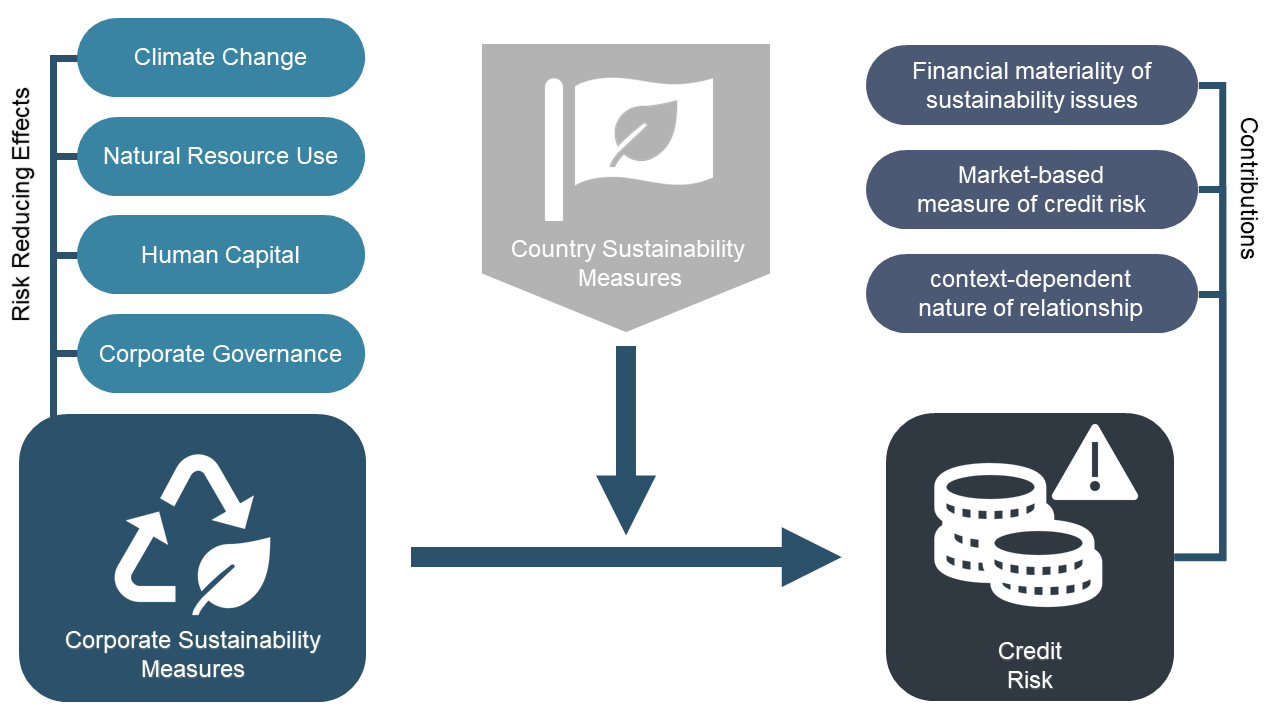

Jrfm Free Full Text Which Sustainability Dimensions Affect Credit Risk Evidence From Corporate And Country Level Measures Html

Derivative Definition

Credit Default Swap Rates For The Italian Republic 5 Years Aug Download Scientific Diagram

Pdf The Valuation Of Credit Default Swap Options

A Credit Default Swap Cds

Solved 7 Which Best Describes A Credit Default Swap A It Chegg Com

2

Pdf On The Relationship Between Asian Credit Default Swap And Equity Markets

Credit Risk Transfer Mechanisms Frm Analystprep

The Credit Default Swap Market And The Settlement Of Large Defaults Cairn Info

Sovereign Debt Renegotiation And Credit Default Swaps Sciencedirect

Comments

Post a Comment